The question used to be simple. Rent until you save enough, then buy.

Not anymore.

In 2026, with interest rates at 5.25% and average UK house prices around £285,000, the decision between real estate investment and renting has become genuinely complex.

Whether you are working with a real estate company to find your first home or browsing rental listings on your own, understanding the long-term financial impact of each choice is critical before signing anything.

This guide gives you the real numbers. You will learn:

- Which option builds more wealth over 5, 10, and 20 years

- The hidden costs most people forget

- How 2026 market conditions change the calculation

- A hybrid strategy you have probably not considered

Let us start with the one thing nobody tells you.

The One Thing Most Advice Gets Wrong

Most “rent vs buy” articles compare mortgage payments to rent payments.

That is incomplete.

The real comparison is between your total unrecoverable costs.

- When you rent, 100% of your rent is unrecoverable

- When you buy, only some of your mortgage is unrecoverable (the interest portion)

Your principal payment is not an expense. It is forced savings.

This single distinction changes everything. Keep it in mind as you read.

For official UK property data, the Office for National Statistics (ONS) house price index provides accurate monthly updates.

Quick Comparison: Rent vs Buy in 2026

|

Factor |

Renting |

Buying (Real Estate Investment) |

|

Monthly payment nature |

100% expense |

Interest = expense, Principal = savings |

|

Upfront cost |

1-2 months’ rent (£1,500-£3,000) |

10-15% deposit (£28,000-£42,000 on average) |

|

Maintenance |

Zero (landlord’s responsibility) |

1% of property value per year (£2,850 on average) |

|

Flexibility to move |

1-2 months’ notice |

3-6 months (plus selling costs at 1-3%) |

|

Long-term wealth |

None from the property itself |

Equity growth + potential appreciation |

|

Monthly cost (UK average 2026) |

£1,200 (one-bed flat) |

£1,500 mortgage (but £700 is principal) |

The key insight: The £1,500 mortgage payment might feel higher than £1,200 rent. But £700 of that mortgage is going into your own pocket as equity. Your true cost is only £800.

For current mortgage rate comparisons, MoneySavingExpert’s mortgage guide is updated weekly.

What Does Real Estate Investment Actually Mean?

There is confusion around this term. Let us clear it up.

Real estate investment does not only mean becoming a landlord with multiple properties.

In this guide, “real estate investment” includes:

- Buying your own home – The most common form. Your primary residence builds equity over time.

- Buy-to-let property – You live elsewhere but own a rental property.

- Property investment funds – You invest in property without buying a whole building.

For most readers, the decision is: “Should I buy the home I live in, or should I rent and invest my money elsewhere?”

That is the question we answer below.

The 2026 Numbers That Matter

The property market has changed. Here is what is different this year.

Interest Rates (2026)

Bank of England base rate: 5.25% (compared to 0.1% in 2021)

Average five-year fixed mortgage: 4.8%

What this means: Borrowing costs are high. Every £100,000 you borrow costs roughly £4,800 per year in interest.

Average UK House Price (April 2026)

£285,000 (up 2.5% from 2025)

What this means: Prices are not crashing. They are growing slowly. Double-digit appreciation is gone for now.

Average Monthly Rent (UK, 2026)

£1,200 (up 8% from 2025)

What this means: Rents are rising faster than house prices. Landlords are passing on higher mortgage costs to tenants.

Average Time to Save a Deposit (First-time buyer)

8.5 years for a 15% deposit on an average home (assuming saving 15% of monthly income)

What this means: Waiting to buy has a real cost. Every year you rent, you pay someone else’s mortgage.

For official rental data, the Gov.uk private rental market statistics page is authoritative.

The Real Calculation: 5-Year Comparison

Let us compare two people with identical incomes and savings.

Person A: Rents and invests elsewhere

Person B: Buys a home

Assumptions (UK average, 2026):

- Home value: £285,000

- Deposit: 15% (£42,750)

- Mortgage: £242,250 at 4.8% over 25 years

- Monthly mortgage payment: £1,500 (approx. £700 principal, £800 interest)

- Monthly rent (comparable home): £1,200

- Annual maintenance (buyer): 1% of value (£2,850 or £238/month)

- Annual investment return (renter’s savings): 5% (stocks and shares ISA)

After 5 Years

|

Renter (Person A) |

Buyer (Person B) |

|

|

Total housing cost |

£72,000 (rent) |

£90,000 (mortgage) + £14,250 (maintenance) = £104,250 |

|

Equity built |

£0 |

£42,000 (principal paid) |

|

Investment portfolio |

£72,000 (if saving the difference?) |

Not applicable |

|

Net position |

£72,000 – £72,000 rent = £0 + investment growth |

£42,000 equity + potential appreciation |

Wait – this is not fair. Person A does not have an extra £72,000 to invest. They paid £72,000 in rent. Person B paid more cash each month but built equity.

Corrected Net Position After 5 Years

|

Renter (Person A) |

Buyer (Person B) |

|

|

Cash spent on housing |

£72,000 |

£104,250 |

|

Equity owned |

£0 |

£42,000 |

|

Investment portfolio |

£0 (no extra cash) |

Not applicable |

|

What you have to show |

Nothing |

£42,000 + 5% appreciation (£14,250) = £56,250 |

Buyer is ahead by approximately £56,250 after 5 years.

This assumes 5% annual appreciation (optimistic for 2026-2031). At 2% appreciation, the buyer is ahead by roughly £36,000.

The takeaway: Buying still wins after 5+ years, but the gap is smaller than in 2021 when interest rates were 1%.

When Renting Makes More Sense

Renting is not “wasting money.” It is paying for flexibility and lower risk.

You should rent if:

- You plan to move within 3 years

Buying and selling costs (stamp duty, legal fees, estate agent fees) typically total 3-5% of the property value. On a £285,000 home, that is £8,500-£14,000. You need at least 3 years of appreciation to break even. - Your income is unstable

Mortgage lenders want proof of stable income. If you are self-employed with variable earnings, renting gives you breathing room. - You are not sure where you want to live long-term

Buying the wrong property because you felt pressure to “get on the ladder” is a costly mistake. Selling a home you have owned for less than 5 years often loses money after fees. - You prefer investing in other assets

Some people genuinely prefer stocks, bonds, or starting a business. Real estate is not the only path to wealth.

For independent advice on renting rights, the Which? guide to renting vs buying is excellent.

When Buying (Real Estate Investment) Makes More Sense

You should buy if:

- You plan to stay for 5+ years

This is the most important factor. At 5 years, buying almost always wins financially. At 10 years, it wins by a large margin. - You want forced savings

Not everyone has the discipline to invest the difference. A mortgage forces you to build wealth automatically. - You value stability

Landlords can sell the property. They can raise rent. They can decide not to renew your tenancy. Owning your home means nobody can ask you to leave (as long as you pay the mortgage). - You want to use leverage

A 15% deposit gives you control of 100% of a property’s appreciation. If the property goes up 3% in a year, that is a 20% return on your deposit. You cannot get that leverage with stocks (without high risk).

The Hybrid Strategy Most People Miss

You do not have to choose 100% one way or the other.

Strategy: Rent in the city, invest elsewhere

Many professionals in London, Manchester, and Bristol use this approach.

- Rent a flat near work. Short commute. Flexibility to move when a job changes.

- Buy a buy-to-let property in an affordable area (northern England, Midlands, Wales)

- Let the rental property pay down its own mortgage while you benefit from appreciation

Real example (2026 figures):

- Rent in Manchester city centre: £1,200 per month

- Buy a terraced house in Burnley for £120,000 with a 25% deposit (£30,000)

- Rental income: £700 per month (covers mortgage and most costs)

- After 10 years: the Burnley house is paid down to £60,000 mortgage and might be worth £150,000

- Your equity: £90,000 from a £30,000 investment

You get lifestyle flexibility AND real estate investment. This is not for everyone, but it works for many.

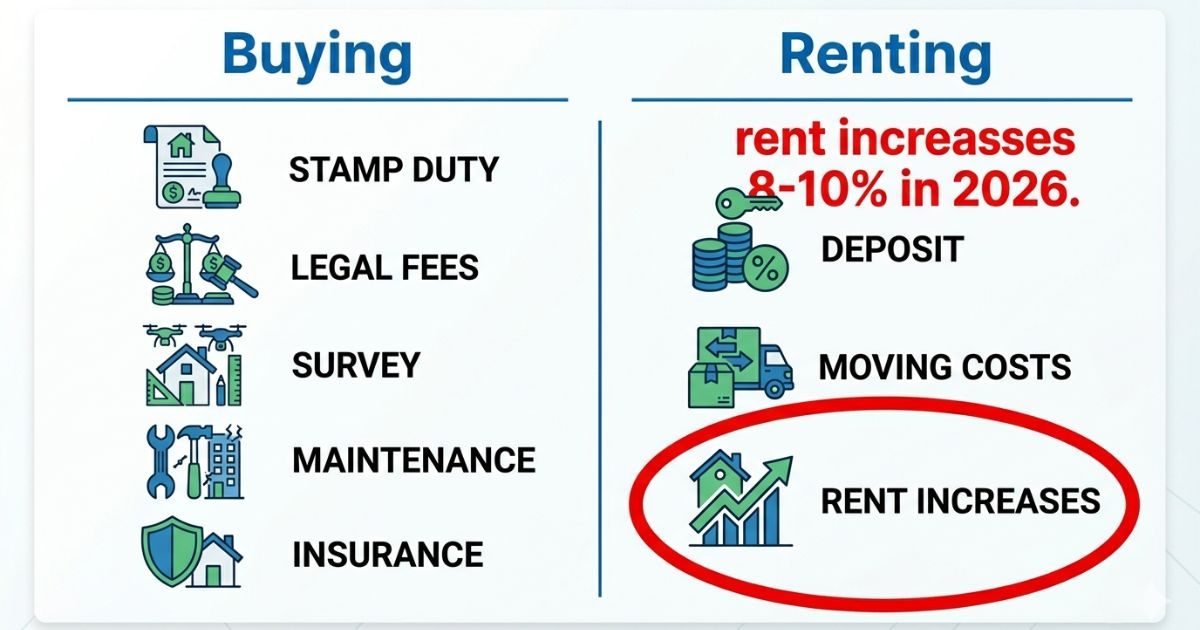

Hidden Costs Most Guides Ignore

Buying (Beyond the Mortgage)

|

Cost |

Typical Amount (UK, 2026) |

|

Stamp duty (first-time buyer) |

0% on first £425,000 |

|

Stamp duty (second home/investment) |

3-5% of purchase price |

|

Legal fees (solicitor/conveyancer) |

£1,000-£1,500 |

|

Surveyor fees |

£400-£1,000 |

|

Mortgage arrangement fee |

£500-£1,500 |

|

Removal costs |

£300-£1,000 |

|

Annual maintenance (1% of value) |

£2,850 (on £285k home) |

|

Buildings insurance |

£150-£300 per year |

|

Ground rent and service charges (leasehold) |

£200-£2,000 per year |

Total upfront buying costs (first-time buyer): Approximately £2,500-£4,000

Renting (Beyond Monthly Rent)

|

Cost |

Typical Amount |

|

Tenancy deposit |

5 weeks’ rent (£1,400 on £1,200/month) |

|

Holding deposit |

1 week’s rent (£280) |

|

Moving costs |

£200-£600 |

|

Rent increases (annual) |

5-10% in 2026 market |

|

No equity built |

£0 |

The hidden cost of renting: Rent increases. In 2026, many tenants face 8-10% increases at renewal. Landlords are passing on higher mortgage costs.

Risk Factors You Cannot Ignore

Real Estate Investment Risks

|

Risk |

Likelihood (2026) |

Mitigation |

|

Property value drops |

Low (supply shortage continues) |

Hold long-term (5+ years) |

|

Interest rates rise |

Medium (Bank of England signals) |

Fix your mortgage rate for 5+ years |

|

Cannot sell quickly |

Medium |

Build emergency fund, do not over-leverage |

|

Major repair (roof, boiler) |

Low but costly |

Maintain 1% annual sinking fund |

|

Bad tenants (buy-to-let) |

Medium |

Use letting agency, reference checks |

Renting Risks

|

Risk |

Likelihood (2026) |

Mitigation |

|

Rent increases |

High (8-10% typical) |

Negotiate longer tenancy (2-3 years) |

|

Landlord sells property |

Medium |

Know your Section 21 eviction rights |

|

No asset growth |

100% |

Invest the cash flow difference elsewhere |

|

Moving costs every 1-3 years |

Medium |

Factor into budget |

Short-Term vs Long-Term: The Deciding Factor

|

Time Horizon |

Recommended Strategy |

Why |

|

1-3 years |

Rent |

Buying and selling costs outweigh benefits |

|

3-5 years |

Either (calculate carefully) |

Depends on local market and interest rates |

|

5-10 years |

Buy (or hybrid) |

Equity + appreciation typically wins |

|

10+ years |

Buy |

Almost always the wealth-maximising choice |

The breakeven point in 2026: Approximately 4.5 years for most UK markets. This is higher than 2021 (3 years) due to higher interest rates and slower appreciation.

Frequently Asked Questions

- Is renting really cheaper than buying in the UK right now?

In monthly cash flow, yes. Rent is typically £300-£500 lower than mortgage payments on a comparable property. But remember: part of your mortgage payment builds equity. The true cost of buying is often lower than renting. - Does buying a home always build wealth?

No. If you buy at the peak of a bubble and sell during a crash, you can lose money. However, UK house prices have increased over any 10-year period since 1950. Long-term ownership is historically safe. - Can renting ever be the smarter financial move?

Yes, for short-term stays or if you invest the money you save. If you rent for £1,000 per month and invest £500 per month into a stocks and shares ISA earning 7%, you could match or beat a buyer’s returns. Most people do not have that discipline. - What is the 5% rule for rent vs buy?

A commonly used rule: If your annual rent is less than 5% of the purchase price of a comparable home, renting is financially better. Example: Rent of £15,000 per year (£1,250/month) vs purchase price of £300,000 (5% of £300k = £15k). At 5%, it is a tie. Above 5%, buying wins. Below 5%, renting wins. - How much deposit do I need in 2026?

Minimum 5% for some government schemes, but realistically 10-15% for good mortgage rates. On a £250,000 home, that is £25,000-£37,500. - Is real estate still a good investment in 2026?

Yes, but with realistic expectations. Do not expect 10% annual appreciation like 2021-2022. Expect 2-4% appreciation plus equity paydown. That still beats cash savings and is more stable than stocks.

For current stamp duty rates, visit the Gov.uk stamp duty land tax page.

Final Thoughts

The real estate investment vs renting debate has no universal answer. But the 2026 market gives us clear signals.

You should probably rent if:

- You will move within 3 years

- Your income is unstable

- You strongly prefer other investments

You should probably buy if:

- You will stay for 5+ years

- You have a stable deposit and income

- You want forced savings and stability

The hybrid strategy (rent where you live, invest elsewhere) works well for many.

The worst decision is doing nothing. Renting indefinitely without investing the difference leaves you with nothing to show for years of housing payments.

Run your own numbers. Use the 5% rule. Talk to a financial advisor if you have complex circumstances.

Your 2026 self will thank you for making a deliberate choice, not a default one.

Author Bio

Henry does not fit neatly into one box and that is exactly why his advice works.

He started his career handling non-fault accident claims, helping drivers fight unfair credit hire charges and insurer delays. After eight years in that world, he retrained as a UK mortgage advisor.

He has since worked with two national lenders and a regional real estate company, guiding clients through property purchases and remortgages.

Today, Henry writes about both fields. He believes where you live and how you travel are the two biggest financial decisions most people make.

His advice has appeared in Auto Express, The Telegraph, and FT Adviser. He lives in Bristol, drives a nine-year-old Volvo, and owns a rental property in the Midlands.